Traditional Providers

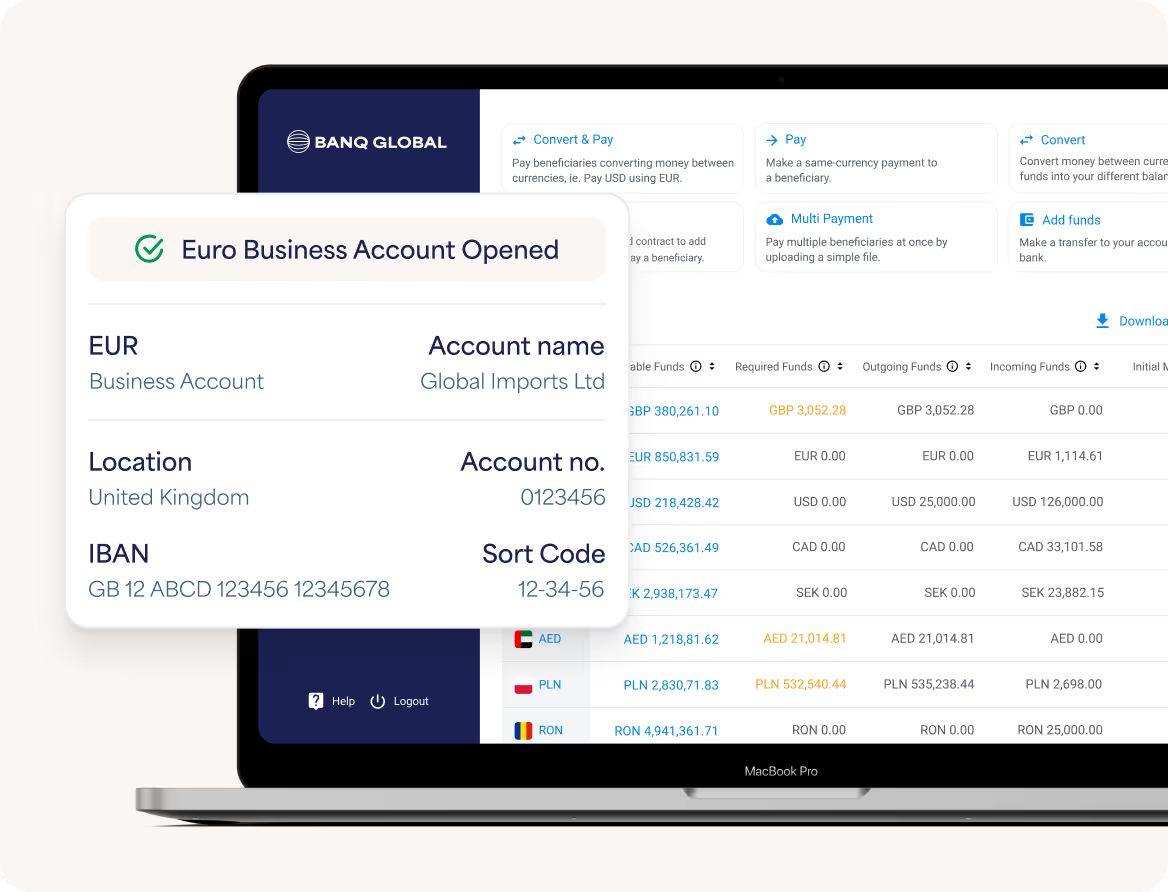

Open a Euro (EUR) Business Account

Operate in Europe with confidence. Banq Global provides Euro (EUR, €) business accounts in your company’s name. Access local and international payment rails to strengthen counterparties' confidence and maintain disciplined control over EUR cash flows.

Reduce FX friction and simplify international transfers

Local EU IBAN details in your company’s name (where applicable)

Access SEPA and SEPA Instant for domestic and regional payments

Suitable for international operations, non-resident directors, and multi-jurisdictional ownership

Euro

Currency name

EUR

ISO code

€

Euro symbol

Why You Need a Euro Account

What’s Included with Your Euro Business Account

A dedicated EUR account embeds your operations into Europe’s local rails, reduces friction with European counterparties, and puts FX timing under treasury policy rather than circumstance.

Key Benefits

Account in your company’s name with unique IBAN and BIC.

SEPA & SEPA Instant for Eurozone transfers; SWIFT for out-of-area EUR.

Receive, hold, convert, and send EUR under clear treasury rules.

Unified platform and responsive specialists for controlled, auditable operations.

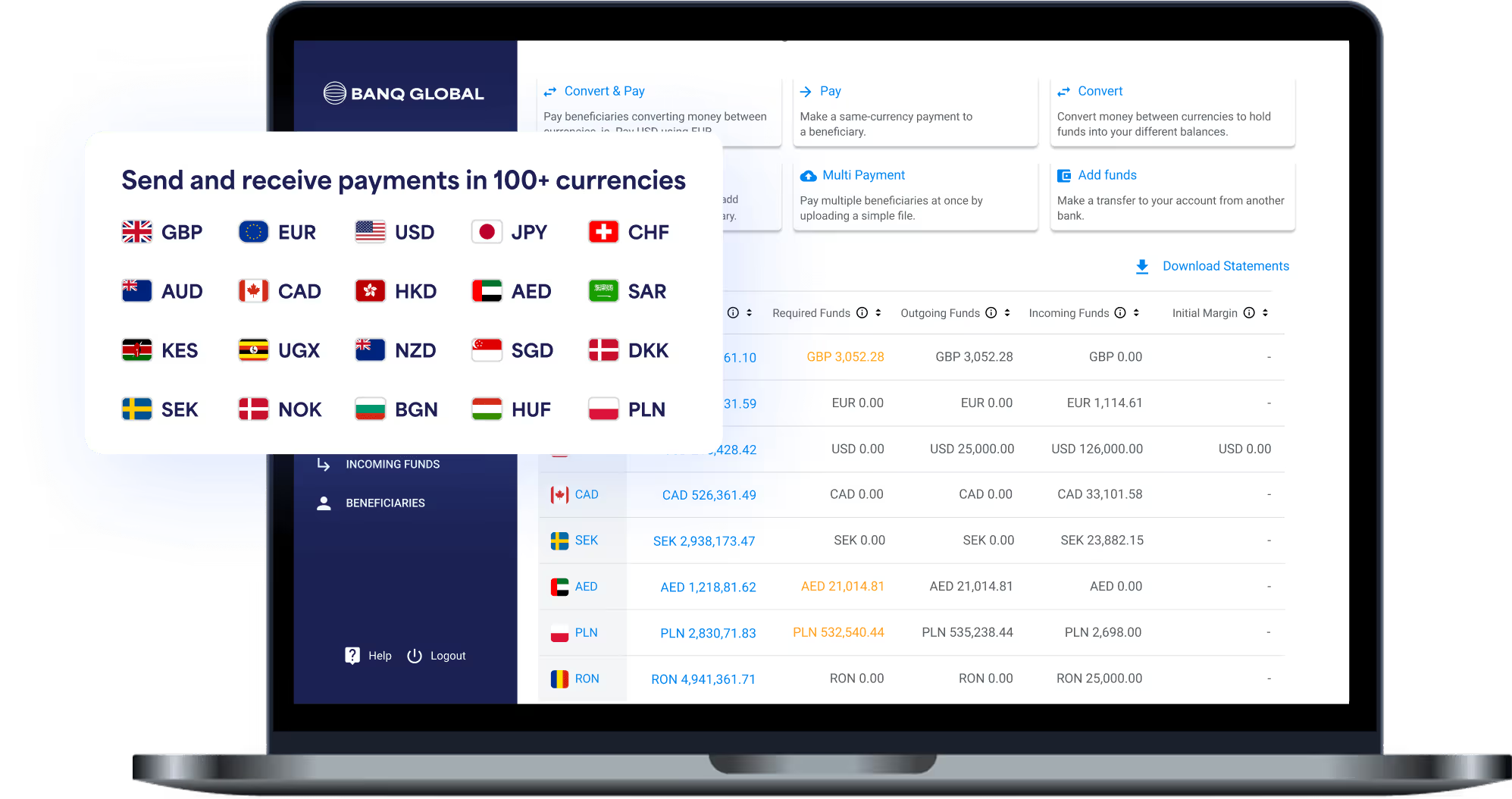

Platform Features

The Risk of Not Having a Euro Business Account

Relying on ad-hoc cross-border wires and forced conversions for European activity introduces cost, delay, and uncertainty. Treasury outcomes become reactive, not controlled.

FX erosion:

Repeated, unplanned conversions compress margins.

Settlement uncertainty:

Correspondent chains add days and fees.

Counterparty friction:

European suppliers prefer local EUR transfers.

Control gaps:

Limited auditability, exceptions, and rework across teams.

Countries Where You Can Open a Euro Account

Corporates demand more than just an account to hold funds. You need precision, visibility, and infrastructure designed for the realities of multi-entity operations, complex ownership structures, and cross-border liquidity management.

(SEPA coverage extends beyond the Eurozone; we’ll advise on the optimal setup for your use case.)

Who We Serve

Our Euro Business Accounts Are Designed for

We support a wide range of internationally minded businesses. From fast-growing companies expanding into Europe to established global organisations managing complex operations.

Global Corporates

Centralise EU receivables, fund suppliers/payroll, and align EUR costs with EUR revenues for cleaner margins.

Explore

Funds & Institutions

Manage capital calls and distributions in EUR with role-based approvals and clear audit trails.

Explore

Private Equity

Efficient EUR flows for deals, fees, and SPV/holdco structures with policy-driven FX.

Explore

Family Offices

Discreet EUR management for assets, commitments, and inter-entity transfers under tight permissions.

Explore

The All-in-One Platform

Banq Global vs. Traditional Providers

Open business accounts (20+ countries)

Open multi-currency accounts (30+ currencies)

Preferential exchange rates (130+ currencies)

Receive global payments (190+ countries)

Make global payments (190+ countries)

Currency risk management

Mass payments

Trade finance

All-in-one platform

Dedicated relationship manager

Business Account - Step by Step

How to Open a Euro Business Account

A clear, expert-led process that reduces rework, shortens decision time, and maintains certainty.

01

Scoping & Fit

Define structure, jurisdictions, directors/UBOs, volumes, and EUR use cases. We confirm feasibility and the optimal configuration.

02

Document Pack

A precise, tailored checklist for your entity type and structure, minimising rounds of clarification.

03

Compliance Review

Disciplined AML/KYC due diligence with prompt Q&A and clear status visibility.

03

Account Issuance

Receive your EUR account in your company’s name with local IBAN/BIC and SEPA enablement.

03

Go-Live & Controls

Users, roles, approvals, payment templates, and FX policy (including market orders) configured to your standards.

Euro Business Account

Operating in Euro (EUR, €) raises detailed questions regarding IBANs, SEPA/SEPA Instant, non-resident onboarding, safeguarding, FX. Here are the direct answers global finance teams ask before opening a Euro business account with Banq Global.